Understanding how a business spreads out the cost of its assets over time is essential to grasp the financial health and operational efficiency of the company. In accounting, this is done through two main processes known as amortization and depreciation. Although they serve similar functions in spreading costs, they apply to different types of assets and have distinct rules and implications for a business’s financial statements.

✅ AI Essay Writer ✅ AI Detector ✅ Plagchecker ✅ Paraphraser

✅ Summarizer ✅ Citation Generator

Every asset a company owns typically has a useful life beyond its acquisition date. Whether it’s a vehicle, a piece of equipment, or a patent, these assets provide benefits over time. To reflect their usage accurately, companies spread out the costs of these assets across their useful lives, a process that not only helps in financial reporting but also has tax implications. This spreading out of cost is what we refer to as amortization and depreciation. Understanding the difference between these two processes is crucial for anyone looking to get a clear picture of how businesses manage their long-term assets.

Amortization: Spreading the Cost of Intangible Assets

Amortization is an accounting technique used to allocate the cost of an intangible asset over its expected useful life. Intangible assets, such as patents, trademarks, and copyrights, have value but lack physical substance. These assets are key to a company’s operation because they can provide an exclusive right or benefit for a period.

Amortization is the financial process of spreading out the repayment of a debt over time through scheduled, predetermined installments that consist of both the principal amount and the interest. This method allows for a debt to be paid off in regular payments, which gradually reduces the principal balance while also covering the cost of borrowing.

In most cases, amortization expenses are spread evenly across the asset’s useful life without consideration for salvage value, as intangible assets seldom have any residual value once they’re no longer useful. The amortization process is straightforward: the same amount gets expensed in each period, usually following a straight-line basis. However, it’s interesting to note that the term “amortization” also pops up in finance, particularly in loan repayment schedules, where it represents the gradual reduction of a loan balance over time.

Depreciation: Accounting for the Decline in Tangible Assets

Depreciation applies to fixed or tangible assets like buildings, machinery, and vehicles. These assets, unlike intangible ones, often have some residual or salvage value at the end of their useful life. To calculate depreciation, the original cost of the asset is reduced by its estimated salvage value, and the remaining amount is allocated over the asset’s lifespan.

Depreciation is spreading a physical asset’s cost over its lifespan, showing value loss over time for tax and accounting purposes, with various methods available for calculating it.

There are several methods to depreciate assets, from the simple straight-line method to more complex ones like the declining balance and double declining balance methods. These methods can result in different expense amounts being recognized each year, which can significantly affect a company’s reported income.

Key Differences

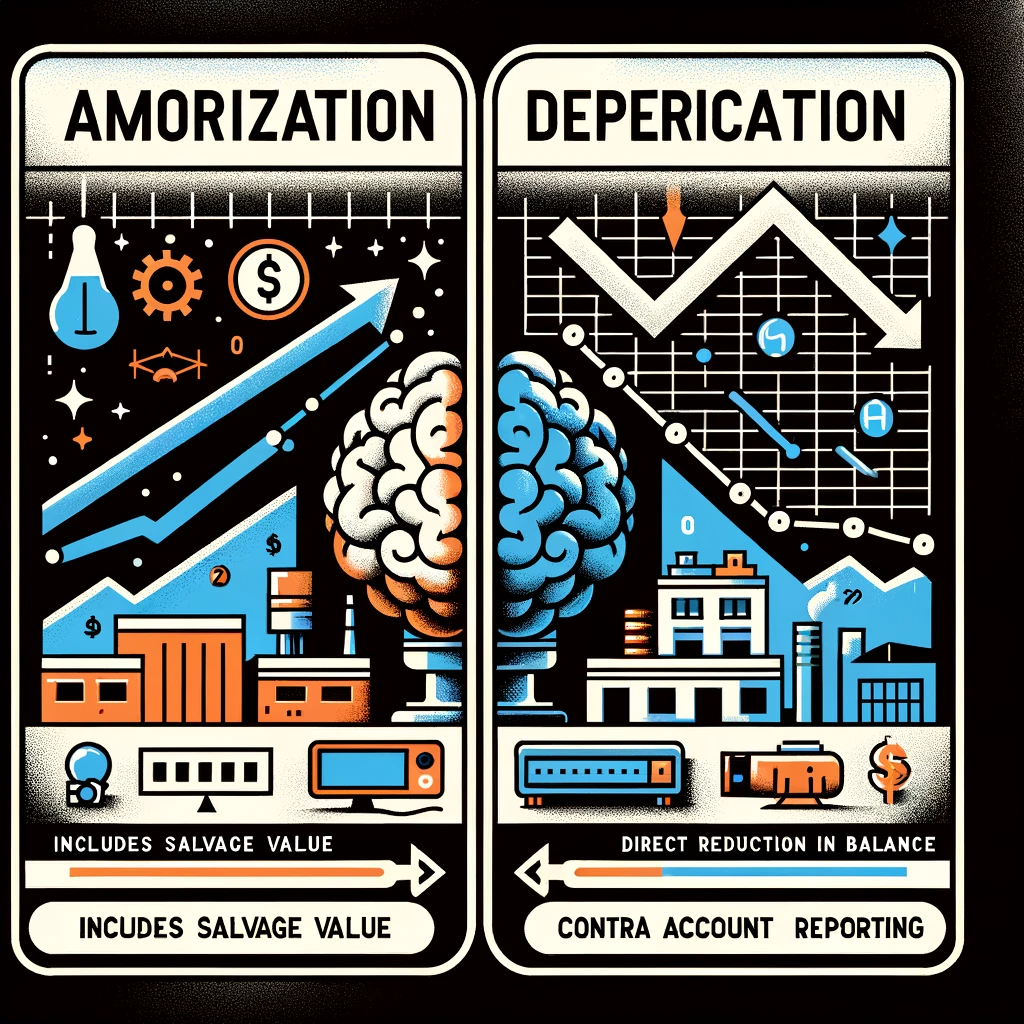

The main distinction between amortization and depreciation lies in the type of asset it applies to. Amortization is for intangible assets, while depreciation is for tangible assets. Moreover, depreciation often includes salvage value in its calculations, reflecting the expected realizable value at the end of an asset’s life, whereas amortization does not, as intangible assets rarely have any value once they expire.

In terms of financial reporting, depreciation expenses are typically reported in a contra account, which offsets the asset’s book value on the balance sheet. In contrast, amortization may not always use a contra account, sometimes reducing the intangible asset’s balance directly.

Both amortization and depreciation are fundamental accounting practices that spread out the cost of an asset over its useful life. They help businesses match expenses with the revenue generated by the asset, comply with the matching principle in accounting, and provide a more accurate picture of a company’s financial health over time. Understanding the nuances between the two can offer valuable insights into how a company manages its resources and plans for the future.

FAQ

More from Accounting Guides

Comments (0)

Welcome to A*Help comments!

We’re all about debate and discussion at A*Help.

We value the diverse opinions of users, so you may find points of view that you don’t agree with. And that’s cool. However, there are certain things we’re not OK with: attempts to manipulate our data in any way, for example, or the posting of discriminative, offensive, hateful, or disparaging material.